Over the past few years, digital currencies designed for stability have become the core infrastructure of the crypto market. From daily trading and global money transfers to decentralized finance (DeFi), they are everywhere. In fact, these digital assets now settle trillions of dollars in transactional volume annually, rivaling traditional payment networks and reshaping how capital moves across borders.

If you are asking what a stablecoin is, you are in the right place. In this guide, we will walk you through the world of Stablecoin, how it works, how to invest in it, and who it is for.

What Are Stablecoins and How Do They Work?

A stablecoin is a cryptocurrency engineered to maintain a fixed value, most commonly pegged 1:1 to a fiat currency like the US Dollar (USD) or the Euro (EUR). While their goal is identical, keeping the price exactly at 1.00, the mechanisms they use to achieve this stability vary drastically.

There are four primary categories of stablecoins operating in the market today:

Fiat-Backed Stablecoins (The Industry Standard)

Fiat-backed stablecoins are the most dominant and straightforward type. For every token issued on the blockchain, the central issuer holds an equivalent amount of real-world assets (cash, short-term government bonds, or commercial paper) in a verified bank account.

- How the peg works: The 1:1 ratio guarantees that users can always redeem their digital token for a real dollar. The system’s integrity relies entirely on the issuer’s transparency and regular independent audits.

- Leading Examples: USDT (Tether) holds the majority of global liquidity, particularly in offshore and trading markets. USDC (Circle) focuses heavily on regulatory compliance, making it the preferred choice for institutions and onshore applications. FDUSD has also emerged as a highly liquid option on major centralized exchanges.Binance’s BUSD also used to be highly popular, but support for it has now been gradually phased out across multiple platforms.

Crypto-Backed Stablecoins (The Decentralized Model)

Instead of relying on real-world bank accounts, these stablecoins use other cryptocurrencies as collateral. Because cryptocurrencies are volatile, these systems require overcollateralization.

- How the peg works: To mint $100 worth of a stablecoin, a user might need to lock up $150 worth of Ethereum in a smart contract. If the price of Ethereum drops drastically, the smart contract automatically liquidates the collateral to buy back the stablecoin and ensure the system remains solvent.

- Leading Example: DAI (managed by MakerDAO/Sky) is the gold standard for decentralized stablecoins, running autonomously without relying on a centralized bank.

Commodity-Backed Stablecoins (Digital Real-World Assets)

These tokens peg their value to physical commodities like gold, silver, or oil.

- How the peg works: The issuer holds physical reserves of the commodity in a secure vault. One token typically represents a specific weight of the asset (e.g., one troy ounce of gold).

- Leading Examples: PAXG (Pax Gold) and XAUT (Tether Gold) allow investors to hold exposure to gold without dealing with physical storage or transport.

Algorithmic Stablecoins (The High-Risk Experiment)

Algorithmic stablecoins attempt to maintain their peg entirely through code, without holding any underlying collateral.

- How the peg works: They rely on smart contracts that automatically expand the token supply when the price goes above $1.00, and burn (destroy) the token supply when the price falls below $1.00.

- Risk Warning: The collapse of TerraUSD (UST) proved that algorithmic models are highly vulnerable to “death spirals” if market confidence breaks. Today, pure algorithmic stablecoins are considered extremely high risk and are largely avoided by serious investors.

| Stablecoin Type | Collateral Backing | Peg Mechanism | Leading Examples | Risk Profile |

| Fiat-Backed | Cash, government bonds, short-term reserves | Central issuer redeems tokens 1:1 for fiat currency. | USDT, USDC, FDUSD | Lowest (Relies on audit transparency) |

| Crypto-Backed | Volatile cryptocurrencies (e.g., Ethereum) | Smart contracts require users to overcollateralize positions. | DAI | Moderate (Exposed to smart contract and crypto asset volatility) |

| Commodity-Backed | Physical assets (e.g., gold vaults) | Tokens represent a specific weight of a physical commodity. | PAXG, XAUT | Moderate (Tied to the underlying commodity’s market price) |

| Algorithmic | None (Uncollateralized) | Computer code dynamically expands or burns supply based on demand. | UST (Collapsed) | Extremely High (Vulnerable to severe de-pegging death spirals) |

The Investment Thesis: Why Hold Stablecoins?

If stablecoins do not increase in value, why do investors allocate massive portions of their portfolio to them?

- Risk-Off Capital Preservation: When the broader crypto market faces a downturn, investors swap their volatile assets (like Bitcoin or Altcoins) into stablecoins. This “locks in” their fiat value without triggering the slow, expensive process of withdrawing funds to a traditional bank.

- High-Yield Passive Income: Traditional bank savings accounts offer negligible interest. By contrast, stablecoins can be lent out to institutional borrowers, traders, and liquidity pools to generate yields ranging from 4% to over 15% APY, depending on the risk tier.

- Cross-Border Liquidity: Stablecoins settle in seconds, 24/7, with fees costing pennies. Freelancers, SaaS platforms, and global supply chains increasingly use them as a superior alternative to SWIFT wires.

How to Invest and Earn Yield on Stablecoins

Generating yield requires moving your stablecoins off a dormant hardware wallet or standard exchange account and deploying them into lending markets. In 2026, yield strategies are split into two distinct ecosystems:

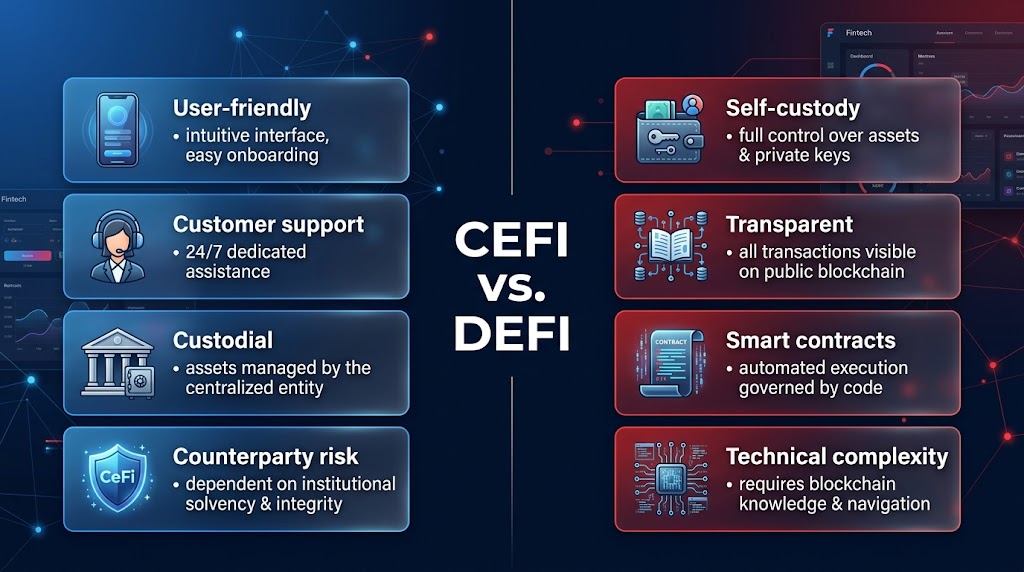

CeFi (Centralized Finance)

You deposit your stablecoins with a regulated corporate entity. The company acts like a traditional bank: they pool user deposits and lend them out to vetted institutional borrowers (like market makers or hedge funds) at a higher rate, passing a portion of the interest back to you.

- Pros: User-friendly, requires no technical knowledge, customer support available, often includes custodial insurance.

- Cons: You must trust the company’s risk management. If the company goes bankrupt, you could lose your funds (counterparty risk).

- Strategy: Look for CeFi platforms that practice strict overcollateralization (demanding borrowers put up more crypto than they borrow) and publish regular Proof of Reserves.

DeFi (Decentralized Finance)

You connect a Web3 wallet (like MetaMask) directly to a smart contract protocol. You deposit funds into a liquidity pool where borrowers take out loans programmatically.

- Pros: Total transparency. You maintain custody of your keys, and all transactions are verifiable on the blockchain. No KYC required.

- Cons: Technical complexity, gas fees for transactions, and the ever-present risk of smart-contract hacks or exploits.

Where to Buy and Deploy Stablecoins for High Yield

The easiest place to buy stablecoins is on major centralized exchanges like Binance, Coinbase, or Kraken, which offer deep fiat-to-crypto on-ramps (via wire transfer, debit card, or ACH). Once purchased, you can deploy them to the following top-tier yield platforms:

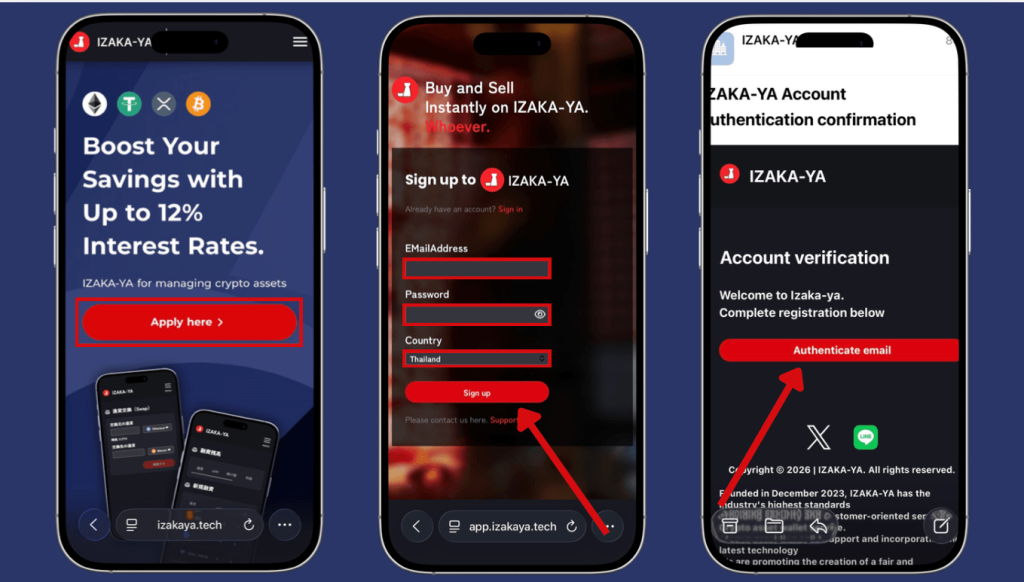

IZAKA-YA (The High-Yield, Frictionless Choice)

- Yield: Up to 33.00% APY.

- Why it stands out: IZAKA-YA functions as an automated passive income engine by providing daily compounding interest without requiring complex Web3 or DeFi knowledge. Security is maintained through a partnership with Fireblocks, employing institutional-grade infrastructure to shield user assets. Crucially, the platform offers a highly frictionless experience with zero KYC onboarding requirements, allowing investors to sign up with just an email address and immediately put their dormant capital to work.

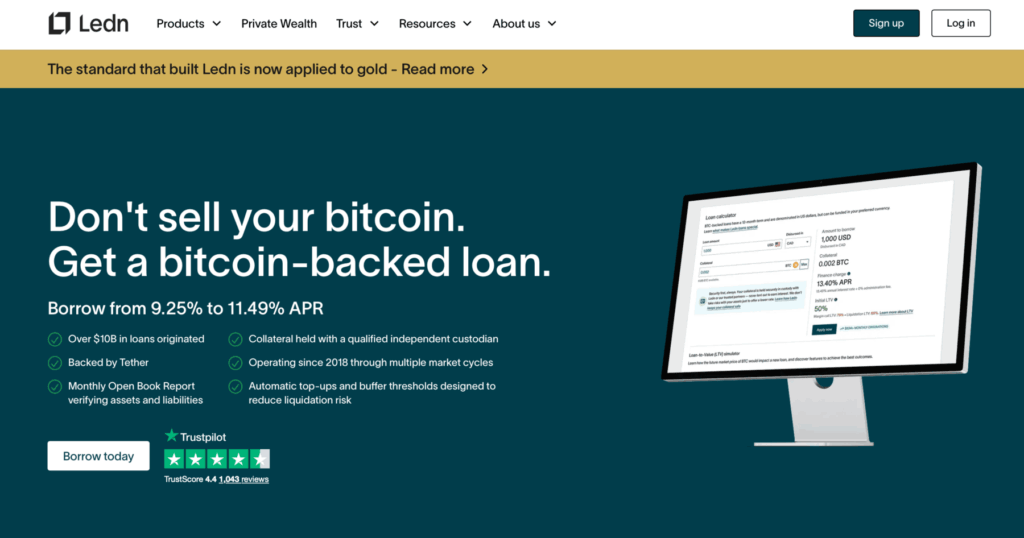

Ledn (The Conservative CeFi Choice)

- Yield: ~6.5% – 8.5% APY on USDT/USDC.

- Why it stands out: Ledn focuses heavily on transparency and sustainable yield. They do not engage in risky, uncollateralized lending. Every loan is overcollateralized, and they provide independent Proof of Reserves audits. With no minimum balance and flexible withdrawals, it is the safest bet for conservative investors who want “set it and forget it” passive income.

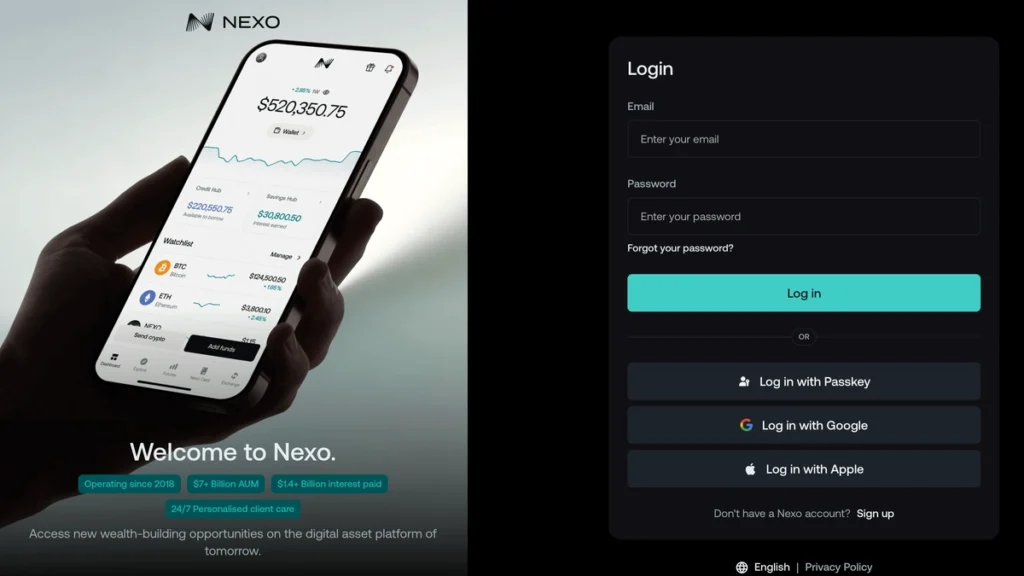

Nexo (The Flexible Multi-Asset Platform)

- Yield: Up to 12.00% APY on USDT/USDC.

- Why it stands out: Nexo offers higher potential yields, but the highest rates require you to lock your funds for a specific term and hold a percentage of your portfolio in their native NEXO token (Loyalty Tiers). It acts as an all-in-one crypto bank, offering yield, credit lines, and crypto-backed debit cards.

Aave V3 (The Institutional Standard for DeFi)

- Yield: ~3.0% – 7.0% APY.

- Why it stands out: Aave is the undisputed king of decentralized lending, boasting tens of billions in Total Value Locked (TVL). Rates fluctuate dynamically based on borrowing demand. Supplying USDC or USDT on Aave is considered the safest play in all of DeFi.

YouHodler (The High-Yield, High-Risk Aggregator)

- Yield: Up to ~15.00% APY.

- Why it stands out: YouHodler offers incredibly high yields, but these come with a distinctly higher risk profile.They cater to aggressive traders who use stablecoins for high Loan-to-Value (LTV) margin strategies. This platform is best for experienced users who understand the counterparty risks involved in maximizing returns.

Alternative Platforms and Innovative Approaches

Beyond standard yield farming, 2026 has seen the rise of platforms integrating stablecoins directly into traditional banking and global liquidity workflows:

- Nebeus (Fiat-Native Bridging): A regulated European platform (Bank of Spain registered) that allows users to take out crypto-backed loans natively in EUR or GBP directly to an integrated IBAN account. It allows users to use stablecoins as collateral without having to off-ramp through a third-party exchange.

- FV Bank: A regulated US digital bank that recently launched a unified fintech platform for stablecoin settlement.It allows B2B businesses to generate invoices and accept payments in USDC seamlessly, converting stablecoin flows directly into traditional banking infrastructure.

- Sovra (MENA Focus): A newer fintech focused on regions with unstable local currencies. It offers self-custodial USD accounts powered by Circle’s USDC infrastructure, allowing unbanked or underbanked users in emerging markets to protect their wealth from hyperinflation while retaining full control of their private keys.

Risks and Regulations

While stablecoins are less volatile than Bitcoin, they are not risk-free. In 2026, the regulatory and operational landscape has formalized significantly:

Regulatory Bifurcation

The market has split structurally into two distinct tiers:

- Regulated/Onshore (e.g., USDC): Fully compliant with European MiCA regulations and US transparency standards. These are deeply integrated into institutional workflows, SaaS platforms, and regulated DeFi lending.

- Offshore Liquidity (e.g., USDT): Operating with more flexibility outside of tightly regulated Western jurisdictions, dominating global trading pairs, and offering unparalleled liquidity in emerging markets.

Key Risks to Monitor

- Counterparty Risk (CeFi): If you deposit stablecoins on a CeFi platform to earn yield, you are an unsecured creditor. If the platform becomes insolvent, your funds are at risk.

- De-pegging Risk: If a stablecoin issuer is suspected of lying about their reserves or if the traditional bank holding their cash collapses, the market may panic. This might cause the stablecoin to drop below $1.00.

- Smart Contract Risk (DeFi): Decentralized lending protocols are governed by code. A bug or exploit in the contract could result in the total drainage of the liquidity pool.

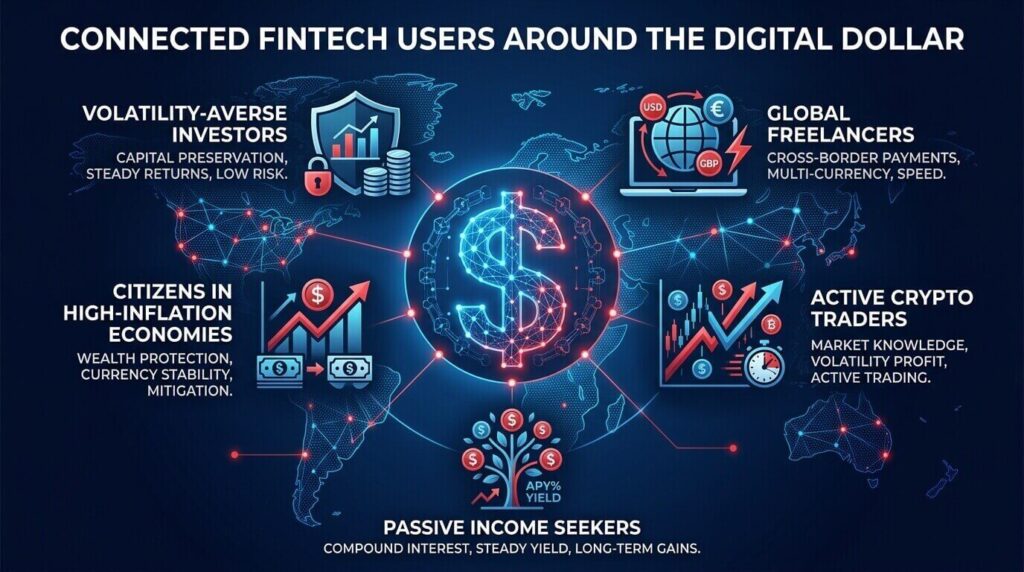

Who Are Stablecoins For?

Stablecoins are no longer just a niche tool for crypto-native traders. They have evolved into a globally adopted financial instrument serving several distinct types of users:

- The Volatility-Averse Investor: For those who want exposure to the high-yield opportunities of the crypto ecosystem but refuse to endure the 30% weekly price swings of Bitcoin or Ethereum.

- Global Freelancers and Remote Workers: Traditional cross-border payments via SWIFT or Western Union take days and carry hefty foreign exchange fees. Stablecoins settle in seconds, 24/7, for fractions of a cent, making them the preferred payment rail for the modern gig economy.

- Citizens in High-Inflation Economies: In countries where the local fiat currency is rapidly devaluing, individuals use dollar-pegged stablecoins as a digital safe haven to protect their purchasing power.

- Active Crypto Traders: Traders use stablecoins as their base currency. When they anticipate a market crash, they sell their volatile altcoins into stablecoins to “lock in” their fiat value, waiting for the right moment to re-enter the market.

- Passive Income Seekers: Traditional savings accounts offer negligible interest. Stablecoin holders can deploy their assets into CeFi or DeFi lending protocols to earn significantly higher annualized returns (APY).

For passive income seekers, rather than allowing your stable digital dollars to sit dormant on a standard exchange, you can utilize yield platforms like IZAKA-YA. By transferring your tokens to the IZAKA-YA crypto lending wallet, you can transform idle capital into a passive revenue engine, securing institutional-grade protection via Fireblocks alongside daily compounding returns of up to 33% APY without any tedious KYC hurdles.

Register IZAKA-YAkeyboard_arrow_rightFrequently Asked Questions

A stablecoin is a cryptocurrency designed to stay at a fixed value, usually one US dollar. Because the price does not fluctuate, you cannot buy it low and sell it high for profit. Instead, it is the perfect tool for preserving your wealth, hedging against market crashes, and earning interest.

While they have drastically lower volatility than Bitcoin, they carry different risks. The main risk involves the transparency of the company holding the cash reserves. This is why investors prefer highly audited options like USDC or USDT.

Standard crypto exchanges rarely pay interest just for holding coins in your spot wallet. To earn passive income, transferring your funds to a dedicated lending platform like IZAKA-YA is a much more profitable choice.

Algorithmic coins have no real money backing them. They rely entirely on computer code to balance supply and demand. If the system fails or investors panic, the coin can rapidly lose its value and drop well below one dollar.

Not at all. The platform is designed to be as user-friendly as your standard mobile banking app. You do not need complex DeFi knowledge, and best of all, there are no tedious KYC verification steps holding you back.